Where does the Greek economy really stand, what do the numbers show, and what do international investment houses expect for 2026.

We are not talking about a simple optimistic forecast, but about a scenario built step by step, with evidence, with data, and with a clearly upward trend.

BUDGET

Let us start with the foundations, the budget. In 2025, Greece did not just meet its targets, it exceeded them by a wide margin. The primary surplus reached €12.6 billion versus a target of €7.6 billion. That is €5 billion more. Tax revenues came in at €64.97 billion, up by €334 million. Spending was lower by around €2.6 billion compared to the plan.

This means the state not only collected more revenue, but also managed its expenses more efficiently. In addition, €2.1 billion was received earlier from the Recovery and Resilience Facility, providing an extra boost.

If we remove the effect of this amount, the primary surplus remains very close to target levels, which points to overall fiscal health.

In other words, Greece is not doing well only on paper. It is doing well in cash terms too.

The question, however, is whether this picture will continue.

The 2026 budget is being built in a different environment. The Recovery Fund is completed by mid 2026, and from 2027 onwards the economy will need to rely more on its own strength.

And this is where the challenges begin. Forecasts point to a slowdown. From 2027 to 2029, average growth is expected at 1.5 percent, compared to 2.2 percent in the previous three year period. The difference is significant.

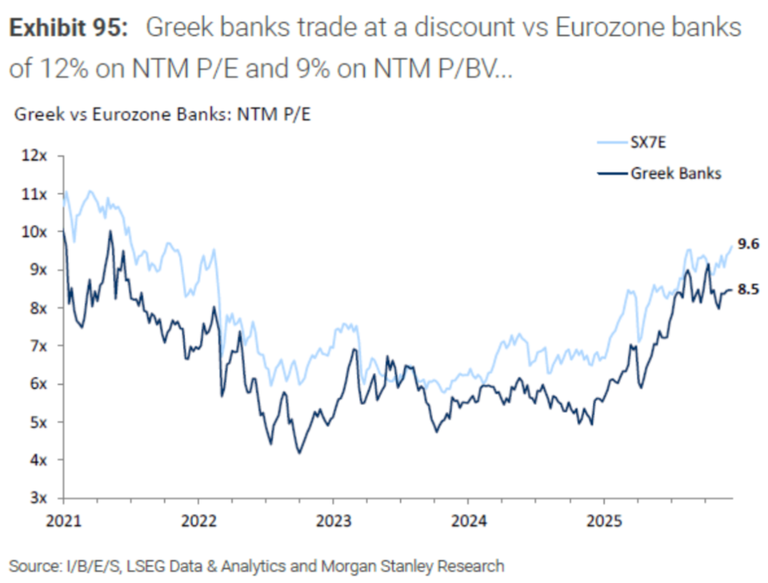

MORGAN STANLEY

Just when one might expect caution, Morgan Stanley comes in and says this: Greece is our top pick in Eastern Europe. And not only that. It sees the positive momentum continuing into 2026 and 2027, with growth of around 2 percent, almost double that of the Eurozone.

The reasons?

First, the Greek stock market performed exceptionally well in 2025, delivering an 82 percent return in dollar terms. Second, Greek equities are still cheap, with the cost of capital falling significantly, from 15.1 percent at the end of 2024 to 11.6 percent during 2025.

And third, the long awaited upgrade is coming. In September 2026, FTSE is expected to upgrade Greece to developed market status. STOXX may follow. All of this translates into institutional capital inflows.

Even if inclusion in the MSCI index is delayed, investors are already starting to position themselves.

Morgan Stanley, however, believes that Greek banks are the main vehicle of the upside. They account for around 75 percent of the MSCI Greece index and have shown remarkable improvement: clean balance sheets, dividends, and strong growth prospects.

The banks’ P/E ratio, meaning price to earnings, could rise from 9.6 to 11 or 12, implying upside potential of 15 to 25 percent. If we also factor in the disappearance of the discount in P/E and P/BV, the upside could reach as much as 40 percent.

And it is not just the banks. Greek bond spreads are narrowing, the euro is strengthening, and consumption is expected to pick up thanks to tax cuts.

Posted Using INLEO